Fraud, like an infection, can stay undetected until the pain is finally felt. And anyone can fall victim.

Bank fraud is as old as the bank itself. It exists together with the financial institutions with each year seeing a corresponding increase with the latest technology.

A report showed that 62% of financial institutions experienced an increase in the volume of fraudulent transactions in 2022 compared to 2021.

Bank fraud has modernized more than just a note handed across the counter by a cashier or a masked gunman brandishing a 6-shooter. The real deal is now done online where hackers break into your account without your knowledge and sweep your account dry.

Banks are seeking solutions to the anomaly caused by these miscreants and how to further detect their activities. But somehow, the ideas are looking like a drop of ink in the sea. In fact, dealing with the surge in fraud and financial crimes is the biggest challenge for 13.5 percent of financial institutions.

So, in this article, we cover preventive measures to adopt to avoid falling victim to these fraudsters.

So let’s jump right into the discussion.

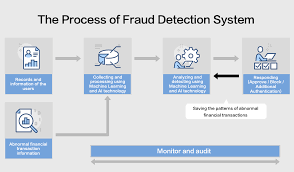

What is fraud detection?

The term fraud detection refers to a strategy or technique used by financial institutions to ensure that assets are secure. In other words, they are the strategies used to identify fraudulent activity and take appropriate action.

Fraud may include:

- The forging of cheques

- Unauthorized access to personal accounts

- Stealing debit or credit cards

Find the best fraud detection software

After having research and scoured the interet, we found SEON to be the best tool. The service you get from Seon fraud fighters is mind-blowing. You cannot even imagine how much better it has become. So let’s look at a few of the advantages listed below.

- It supports e-mail, location, IP and phone analysis.

- It consists of login authentication, behavior analytics and detecting multi-account use.

- Applicable in machine learning as it makes use of Graphical User Interface (GUI).

- It promotes custom rules and allow for browser extension.

- It boosts API and fraud detection.

Types of banking fraud

Banking fraud exists in different forms as each breaking day sees a new change developed by these fraudsters. We outline the most commonly used ones here so you don’t fall victim to them.

- Loan fraud

Loan fraud is when criminals use your personal details to obtain a loan from financial institutions or banks and the responsibility for repayment lies within your care. This is shocking to hear, right?

Imagine you wake up one morning, receiving a call from your bank alerting you that your loan repayment date is due. This is the real shocker.

But it’s possible, and it happens. All their intention is to defraud you and they will explore all available routes to ensure that is possible. This is why concealing your personal info is highly recommended.

- Account takeover (ATO)

This is a type of bank fraud where a criminal takes full charge of a personal account with the assistance of a bot.

They employ different attacks like ransomware, malware, and phishing. Account takeover is also the unauthorized access by criminals to a person’s account.

- False identity

Non disclosure of identity is a bank fraud as this gives the bank zero knowledge about the user. Normally, fraudsters will always want to disguise their identity so that after committing a crime, they won’t be caught.

So, in the effort to achieve this, they try to create a pseudonymous account without disclosing their identity.

- Money laundering

Money laundering is the act of engaging in transactions designed to obscure the origin of money, especially money that has been obtained illegally.

Money is acquired, transaction takes place but they are hidden so it’ not traceable. The money launderer tries to transact little by little with the money, unnoticeable by the bank.

7 Rules to prevent banking fraud

The banking industry is currently a target for fraudsters. Cybercriminals are constantly coming up with new schemes to defraud banks, even the most proficient banks are not spared in this attack.

With unlimited ways to commit fraud, fear has gripped the minds of banks and other financial institutions as to how to protect the assets entrusted with them.

However, you can follow these easy steps to reduce fraud by spotting it and taking the necessary action to prevent it from happening.

- Create a strong password

Creating a strong password is the first and foremost requirement. Passwords and multi-factor authentication are the defenses against fraudulent activity. Hence, you must use a secure password on your device and enable two-factor authentication.

Through the use of your phone number or email address, the two-factor authentication will send you a code to confirm your access before signing in to the account.

It’s also advisable to use different passwords on different accounts. Never use commonly known passwords like 12345 or QWERTY, and change your password regularly.

- Educate your employees

Your employees are at the forefront of the detection of fraud. Ignorance can cause so much damage and breach of data when people are unaware of what to do, what to expect, and the consequences of any action they take. Train them on the red flags and other ways fraudsters operate.

Also, teach them how to recognize and avoid phishing scams. Phishing messages are one way scammers trick people by making them disclose sensitive information about themselves.

Furthermore, it’s a good idea to educate your customers so that they know how to respond to phising emails when they see such so as to avoid falling victim.

- Perform internal audits

It’s necessary to perform a thorough audit of your finances. Internal audits and performance reporting are tools for detecting fraud.

It reveals the point where cash has been misappropriated and traces it to the defrauder. Think about speaking with a trained fraud examiner rather than just performing an accounting audit.

- Embrace artificial technology

The world is fast growing and is seeming as though human capacity cannot catch up with the current wave. So in that stride, a non-human factor has been introduced to augment the lapse created in the quick surge.

Nowadays, this artificial technology can help detect the activities of a fraudster even though he is using a hot. There are bot management softwares and all these are AI developed overtime before the rising fraud activities. Some of the techniques used in AI to detect fraud include, data mining, neural networks, machine learning, and pattern recognition.

- Impose the use of personal login information for IT administrators

It is challenging to keep track of IT administrators’ behavior because they frequently log into network infrastructure using generic logins. It should be necessary for these workers or contractors to log in using their identities to provide an audit log.

In addition, monitor access control credentials regularly. Keep an eye out for warning signs, such as staff who are more accessible than they should be, and review records to see if anyone has gotten a temporary extension of accessibility that would make it simpler for them to commit fraud.

- Utilize tools for real-time data enrichment

Real-time data enrichment adds consolidated, supplemental data from other sources, like open-source databases, digital services, and social networks, to the KYC records of consumers because it gives you more information.

Furthermore, it makes you learn more about your users without requesting their personal information. You can combat fraud as a response without compromising seamless customer experiences.

- Use the right tools and resources

With so much assistance and offers by fraud fighters, you have a sure bet of safety from those defrauders. As scammers are growing in skills and tactics, more and more technology is emerging to outsmart their intelligence. These fraud fighters provide excellent service for fraud detection.

With this point mentioned here, you might already be thinking about the fraud fighter that offers the best solution for fraud detection. Look no further, as Seon is here for you.

Fraud prevention: how it works

There are plenty of tools available that act as fraud prevention for businesses with a high-risk tech stack. Preferably one that is flexible and available.Find fintech firms, like Revolut, NuBank, and Mollie, and discover who they’re using. If the best are using them, then why not your company too?

Common uses of fraud prevention tools:

- Identify and stop fraudulent activity,

- integrate social indicators with data from digital footprints.

AI and machine learning are adaptable to the various ways organizations assess risk.

Fraud detection tools operate in the background to give customers a seamless experience while preventing fraud with speed, size, depth, and breadth.

Find a tool to reduce the costs, delays, and challenges caused by fraud for online businesses. Whether you run a small e-Commerce startup or a huge global corporation, this technology makes fraud control simple so you can concentrate on expanding and developing your business.

It’s a wrap

Nowadays, cyber attacks on banks is becoming inevitable because each day sees a new technology and these fraudsters are taking advantage of it to develop their profitiency.

Thus, it has become more urgent than before for banks to stay on their foot in dealing fraud and detecting their activities.

Notably, by using these straightforward techniques, you are on your way to uncovering any fraudulent activity within your company.